History of Financial Difficulties

District Funds

Chartiers Valley’s “general fund” can be thought of as the district’s combined checking and savings account. Revenues are put into the account each year, expenditures are withdrawn, leaving a balance of reserve savings for unaccounted or unexpected expenses.

General Fund - The General Fund is the general operating fund of the School District. It is used to account for all financial resources except those required to be accounted for in another fund. Normal debt service payments for general long-term debt are recorded in the General Fund by the School District.

Capital Improvement Fund – The Capital Improvement Fund is the School District’s construction and capital reserve funds and accounts for funds which are typically borrowed and used for major capital improvements.

Debt Stabilization Fund – The Debt Stabilization Fund is used to pay for future long term debt Obligations.

The other governmental funds of the School District account for other resources. They include the district activities fund and the concession stand fund of the School District whose uses are restricted to particular purposes. Expendable trust funds are also accounted for as governmental funds. These are funds in which both the principal and earnings are available for expenditures. The School District maintains one of these funds: the Designated Trust Fund

From 2015 - 2025, the average yearly expenditures (the cost to run the district) was around $70 million. At the end of each year, the general fund contained an average of $4.5 million acting as a safety buffer, representing about 7.5% of the district’s overall budget. For reference, personal finance experts often recommend keeping three to six months of expenses in an emergency fund. If applied to the district, this would be $17.4 million - $35 million in the general fund. While the reserves kept by commercial entities differ by sector, the general advice of three to six months of expenses still applies. Simply put, Chartiers Valley has only been able to maintain an extremely thin margin of reserves for many years.

School Taxes & Income

The primary source of funding for schools in Pennsylvania are local property taxes. There are state and federal contributions to the overall budget, however they’re a tiny fraction of the overall operating budget year over year.

In Pennsylvania, school boards possess the power to raise property taxes with a majority vote. Act 1 of 2006 limited the board's ability to raise taxes above a specific percentage from the previous year. School districts can propose tax raises over this threshold to be voted on by community members. With voter approval, districts can raise property taxes.

Rates are set as a percentage of property value known as mileage. To calculate owed yearly tax, you multiply the value of your property by the mileage rate set by the district. One mill is equal to one thousandth of a dollar. For example, if a property is valued at $200,000 and the mileage that year is 20.1909, the formula becomes (200000*20.1909)/1000 = $4,038.18 tax due.

Keep this in mind as you continue to read through this page. The district works themselves into a corner due to refusal to raise taxes.

Here are the Chartiers Valley School District tax rate changes over time according to Allegheny County records:

| Year | Mileage | Percent Change | Notes |

|---|---|---|---|

| 2001 | 16.25 | ||

| 2002 | 16.25 | 0% | |

| 2003 | 18.6 | 14.46% | |

| 2004 | 16.25 | 0% | |

| 2005 | 16.25 | 0% | |

| 2006 | 16.25 | 3.87% | |

| 2007 | 19.32 | 0% | |

| 2008 | 19.32 | 0% | |

| 2009 | 19.32 | 0% | |

| 2010 | 19.88 | 2.9% | |

| 2011 | 19.88 | 0% | |

| 2012 | 19.88 | 0% | |

| 2013 | 16.2175 | -18.42% | |

| 2014 | 16.2175 | 0% | |

| 2015 | 16.2175 | 0% | |

| 2016 | 16.6067 | 2.4% | |

| 2017 | 16.6067 | 0% | MS/HS campus construction begins |

| 2018 | 17.071 | 2.8% | |

| 2019 | 17.5595 | 2.86% | |

| 2020 | 18.2118 | 3.71% | |

| 2021 | 18.758 | 3% | |

| 2022 | 19.3957 | 3.4% | |

| 2023 | 20.1909 | 4.1% | |

| 2024 | 20.1909 | 0% | |

| 2025 | 20.1909 | 0% | 2025 furloughs |

School Bonds

School districts are able to take out bonds (loans) to finance large projects like capital improvements to structures. A bond is sold to investors in return for repayment of the principal and interest over a period of 12 - 20 years. The repayment for the bond comes from property taxes in the case of Pennsylvania.

The process is similar to taking out a personal loan to renovate your house. You take out the loan, you make the improvements, and over a predetermined period of time you pay it back using your income.

In Pennsylvania, school districts are required to hold elections to seek approval for bonds. A simple majority of voters is required for the bond measure to pass. This process ultimately ensures the community members that will be on the hook for the bond repayment (via property taxes) are aware and in agreement of the long term investment.

Construction Funding

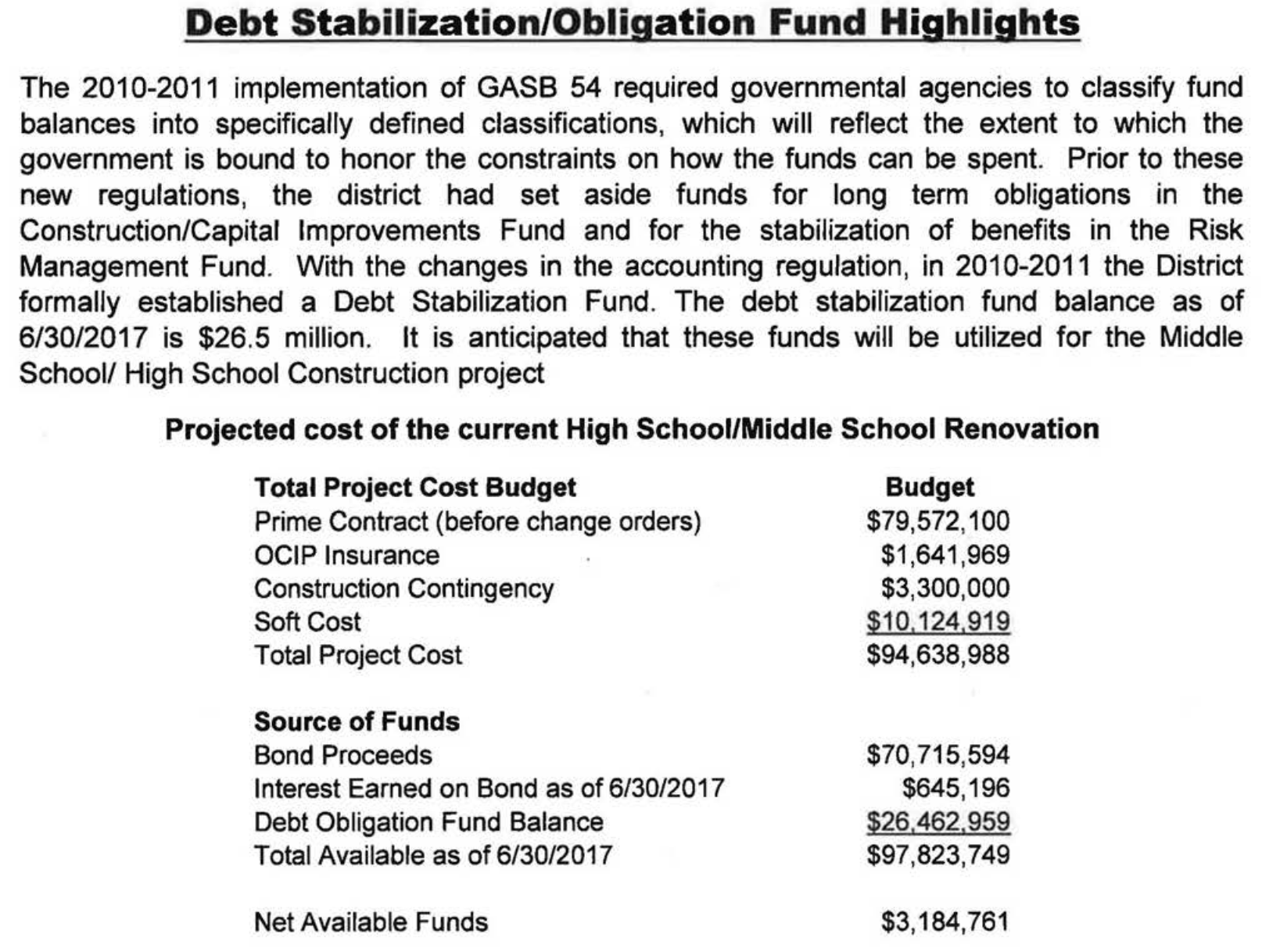

With the district aligned on the need for a new campus in 2016, it became time to determine funding allocation for the project. The district and its contractors expected the entire project (middle and high schools plus additional refurbishments) to cost $94,638,988 in 2017 dollars. The primary source of funding of the project would come from bonds totaling $70.7 million with the rest of the bill paid from the reserves of the Debt Obligation Fund.

The district approved $88.5 million dollars in 2017 for the construction of the new campus and renovations of the theater. A groundbreaking ceremony was held May 31, 2017 in the theater to commemorate the next step in the district’s evolution.

In place of using the district’s general fund, a specific construction fund was established to cover the costs of building the new campus.

The Construction Fund was established to build the new Middle School and renovate the existing High School. This Fund began the 2016-2017 school year with a fund balance of $49.3 million. In 2016-2017 interest earnings provided additional revenue of $.3 million and the issue of additional bonds also added $15.4 million to the construction fund.

Several audits of the district mention the opening balance of $49.3 million dollars. We believe those bonds were issued in 2015 and 2016 in multiple parts.

General Obligation Bonds, Series A of 2015 were issued in the amount of $18,240,000 to current refund the School District’s Series A of 2004 Bonds. The Series A Bonds have variable rate interest from 1.00% to 5.00% with final payment due in fiscal year 2028.

General Obligation Bonds, Series B of 2015 were issued in the amount of $51,870,000 to be used for the renovations, additions and improvements to the Middle/Senior High School Complex. The Series B Bonds have variable rate interest from 3.125% to 5.00% with final payment due in fiscal year 2045.

General Obligation Bonds, Series of 2016 were issued in the amount of $15,350,000 to be used for the renovations, additions and improvements to the Middle/Senior High School Complex. The Bonds have variable rate interest from 1.05% to 4.00% with final payment due in fiscal year 2047.

During June 2021, the School District issued Series 2021 General Obligation Bonds in the amount of $32,530,000 to currently refund a portion of the Series B of 2015 Bonds. The Series 2021 General Obligation Bonds bear interest at rates ranging from 0.20% to 2.96%. Payments are due semi-annually on the Series 2021 General Obligation Bonds through October 2040. The refunding resulted in an economic gain of approximately $2.7 million and cash flow savings of approximately $3.5 million.

During November 2021, the School District issued Series 2021A General Obligation Bonds in the amount of $16,830,000. The bond proceeds will be used to pay the costs of acquiring and constructing repairs, renovations, alteration, and improvements to the School District’s High School Complex, Primary Center, and Intermediate School. The Series 2021A General Obligation Bonds bear interest at rates ranging from 2.00% to 3.00%. Payments are due semi-annually on the Series 2021A General Obligation Bonds through October 2050.

The General Fund has been used in prior years to liquidate the liability for long-term debt. The School District has established a debt stabilization fund to assist with long-term debt payments as needed.

By 2018, the construction fund had been depleted as expected by the administration. Moving forward the district would instead transfer funds from the district’s Debt Stabilization Fund to cover incremental construction costs. At this time it was anticipated that the Debt Stabilization Fund would fully cover the anticipated construction costs.

As planned in June of 2018 when Construction cost exceeded the funds available in the Construction fund a transfer of $1.7 million was made from the Debt Stabilization/Obligation Fund. It is anticipated that the remaining construction cost will be funded by the Debt Stabilization Fund.

The following is a breakdown of the certified audit balances of the various funds the district utilizes for normal operations, capital improvements, and debt obligations. In 2015 and 2016, multiple rounds of bonds were issued to finance $85,460,000 of cash flow to the district. By 2018 - 2019, that $85 million had been spent almost entirely on the construction of the new campus. As the bonds are required to be spent on specific categories of improvements, this was expected. Around the same time in 2019, the district began pulling funds from the Debt Stabilization Fund and the General Fund to continue financing ongoing construction. As of 2024, certified audits show both the General and Debt Stabilization Funds having less than $3 million each.

| Year | General Fund Balance | Construction Fund Balance | Debt Stabilization Fund Balance |

|---|---|---|---|

| 2016 | $2,286,278.00 | $49,300,000.00 | ? |

| 2017 | $2,433,437.00 | $25,800,000.00 | $26,500,000.00 |

| 2018 | $4,516,141.00 | $500,000.00 | $25,000,000.00 |

| 2019 | $1,486,650.00 | $11,237,014.00 | $11,263,831.00 |

| 2020 | $2,925,777.00 | $3,224,646.00 | $5,535,818.00 |

| 2021 | $7,070,396.00 | $3,833,414.00 | $3,846,914.00 |

| 2022 | $6,792,260.00 | $17,573,227.00 | $3,852,305.00 |

| 2023 | $7,116,095.00 | $16,553,295.00 | $3,996,254.00 |

| 2024 | $8,157,443 | $12,607,839 | $3,572,750 |

| 2025 | Not yet audited | Not yet audited | Not yet audited |

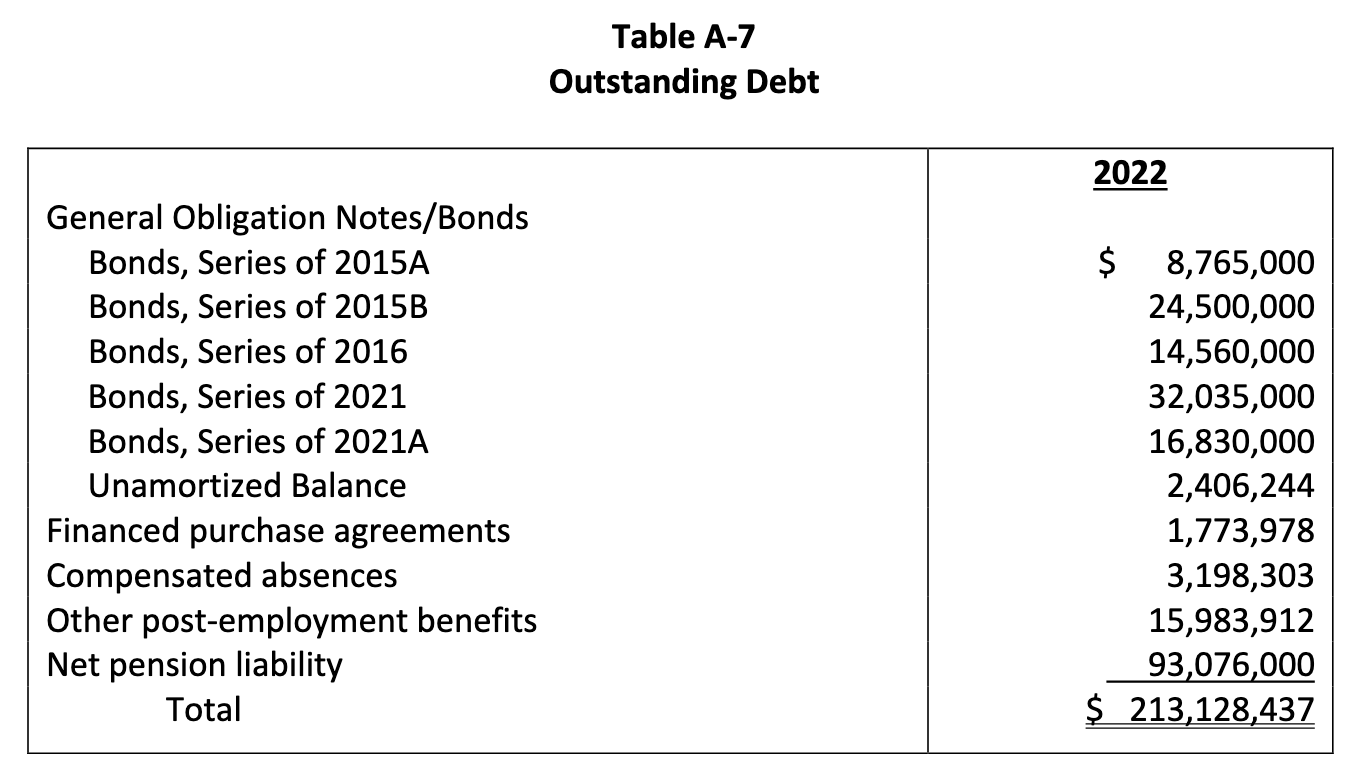

Like any loan, bonds are repaid over time including the compounding interest. As of 2022, the bonds issued in 2015 and 2016 for construction totaled $47,825,000 in debt. Additional bonds taken out in 2021 totaled an additional $48,865,000. As of the 2022 audit, the district had a total outstanding debt of $213,128,437 that would continue to be repaid throughout 2050. For reference, 2022’s total revenues for the district totaled $72,374,493.00.

2025 Furloughs and Cost Cutting

On 2/25/25, the board held a regularly scheduled board meeting with an agenda item of furloughs. The district approved (article 1 / article 2) the elimination of multiple positions in an effort to save the district from a multi-million dollar deficit amid depleted reserves. The following is an excerpt from auditor findings:

The District forecasts that there could be a maximum number of 20 professional employees providing direct instruction to students, 8.47% of the applicable category, suspended pursuant to 24 P.S. §1124(a)(5). This number is subject to bidding rights under the Collective Bargaining Agreement.

Significant structural budget deficits exist; they cannot be corrected through tax increases alone within the Act 1 Index. Although other opportunities for expense reduction have been developed and faithfully implemented over multiple years, and although the District raised the millage rate each year between 2018-2019 and 2023-2024, the District’s fund balance has decreased and, to reduce the reliance on fund balance for the 2025-26 year without the proposed suspensions, the total fund balance will be largely depleted.

Without the proposed suspensions, the District currently projects a deficit for the 2025-26 year. Specifically, the School District’s 2024-25 budget projections show revenues of $76,517,672 and expenses of $80,694,873 with a projected ending fund balance of $5,998,908 ($1,757,199 Unassigned). In addition, the School District’s 2025-2026 budget is projected to show revenues of $76,471,977 and expenses of $81,618,976 with an ending unassigned fund balance in the amount of $247,053.

The projected expenditures of the District for 2025-2026 without the proposed suspensions are $81,618,976. The projected expenditures of the District for 2025-2026 with the proposed suspensions are $79,007,359. The remainder reductions necessary will come from adjustments to staffing and non-staffing costs in other areas.

The projected total revenues of the District for 2025-2026 is $76,471,977.

It is estimated that, with the proposed reductions, including professional employees providing direct instruction to students in the 2025-2026 school year, the School District’s 2025-026 budget will show revenues of $76,471,977 and expenses of $79,007,359 with a remaining unassigned fund balance of $1,004,422.

Prior to the board meeting, a district principal Dr. Lesley McDonough sent an internal email to district employees threatening retaliatory action should they be caught encouraging students to attend the board meeting. The district would later disseminate an update via ConstantContact attempting to clarify the email. The “clarification” reinforced that the principal has the authority to enforce board policies and that the principal's email was justified. It did not, however, touch on policy 321 not prohibiting such actions. The district provided no further interpretation of the policy. The ordeal caused significant controversy within the district.

At the conclusion of the 2024 - 2025 school year, the general fund balance was $5,998,908.00. Looking at the 2025 - 2026 anticipated budget, expenditures not covered by revenue (should the district continue to operate as normal) was $5,146,999.00. If the furlough plan was to be implemented as presented, the uncovered balance would drop to $2,535,382.00. Both options for the 2025 - 2026 budget result in funds needing to be transferred from the district’s general fund, their last line of reserves for yearly operation.

Without furloughs, the general fund balance would be depleted to $851,909.00, a nearly inoperable amount of financial wiggle room for the district. The furlough plan would reduce the need for $2.6 million dollars from the general fund, leaving the anticipated final general fund balance at $2,535,382.00. The second lowest actual general fund balance was $1,486,650.00 at the conclusion of the 2018 - 2019 school year which was the first year of full blown new campus construction.

The resolution mentions “Significant structural budget deficits exist; they cannot be corrected through tax increases alone within the Act 1 Index.” This refers to the 2006 Act 1 that limits the year over year property tax increases by school districts without voter approval. The district here is saying that even if they were to maximize the property tax increases within their power, it would not resolve the forecasted deficit. It could be resolved by voter-approved raises, however in the current political and economic climate the district may feel this is unlikely to pass. If the increase were put to a vote and the vote does not fall during regularly scheduled special elections, the district would be financially responsible for the costs associated with running the election. With forecasted doubt, incurring additional cost with the prospect of only losing money may not be favorable.

The district board voted not to increase tax rates in 2024. One dissenting board member expressed concern over what would become the reality leading to the furloughs:

I voted against the budget because I don’t think it addresses the district’s difficult financial situation in either the short term or long term,” Montani said. “The district has a budget deficit of nearly $2 million, which will be filled entirely through the district’s fund balance. It doesn’t increase revenues or cut costs. It simply hurts our nest egg. In my view, this is not a sustainable solution.

2025 would bring about the very scenario Montani was concerned with. As explored above, the district would be forced to use reserve funds from the general fund. Without the furloughs, the funds would be left with almost nothing. The board was backed into a corner of their own making.

Let’s revisit property tax increases and Act 1. The 2023-2024 Act 1 maximum increase percentage was 4.1%. In 2023, revenues from property taxes totaled $54,317,514. At time of writing, 2024 and 2025’s audits have not been certified. However, 2024 and 2025 brought 0% in mileage tax increases. While not a perfect calculation as it does not account for property value appreciation, we can estimate the 2024 and 2025 local revenues for the district to be around $55 million. If we were to instead apply the maximum percentage increase of 4% permitted by Act 1 in 2024, $2.2 million in additional property taxes would be collected. The amount projected to be saved that necessitated furloughs was $2.6 million. Had the district raised taxes in 2024, furloughs would not have been necessary. It would not have alone solved the deteriorating financial position of the district, but it would have softened the landing into deficit spending.

The community showed a strong show of support for the educators and staff positions being eliminated, however it’s important to point out that voting to not raise taxes and pressuring the board not to do so directly resulted in the furloughs.